How do you even begin to figure out how much you need to save to retire early (or at all)? In this post, I’ll talk about a simple way to estimate how your money might grow as you save toward FIRE and then deplete as you spend it in retirement. I’ll show this with an excel model, but don’t fear if the thought of a spreadsheet is terrifying. I readily admit that, having been trained as a lawyer, all but the most rudimentary of financial modeling is well outside my wheelhouse. Fortunately for me – and you – the modeling we’ll talk about below falls squarely into the category of about as rudimentary as it gets while still actually showing you something.

Before we get to the illustration, let’s talk first about the different ways to save and invest for early retirement. The first approach is to save as much as you can haphazardly and kind of see how it pans out. And that works for many people – if you have the discipline. Remember that it’s very tempting to deviate sometimes. Imagine you’ve just received your paycheck, or your bonus, and you’ve been doing a good job saving and investing, and you think – what if I just take a $1,000 and go crazy. Ultimately there may not be much harm in that. We all need to live sometimes and the benefit of doing that far outweighs a long-term goal.

The problem is doing that too much – especially if you’ve done it once. That first $1,000 or whatever ends up happening again, and again, and before you know it, you’ve re-directed $6,000 in a single year that you intended to save. If you’re 30 when you do that, and you consider the amount of growth you’ll miss out on, it adds up. This is why 401(k)s work well – you never see the money in the first place.

What tends to work better than haphazard saving is the second approach: setting specific goals so that you can understand exactly what you need to strive for to attain your goal. It might even be simpler than that – sometimes doing the math can give you a true reality check of whether early retirement is possible to begin with. And sometimes it can help you figure out if there’s something you need to be changing, such as your spending habits, your job, or anything that might affect your finances.

Below I’ll show one example of calculating income growth up to the point of retirement, and thereafter how that money will decline as you live off it. Remember that it’s not as simple as just reaching a peak – everything is dynamic. Even as you spend money in retirement, the remainder of the money still grows; meanwhile, inflation will eat away at your spending power. These and other variables have to be accounted for.

Keep in mind that a calculation of this type will inherently contain some generality. Even if you plan every single expense for the rest of your life – including every unexpected roof leak and flat tire – you’ll still be far from reality. We have to make assumptions that we can’t possibly get correct – if you had that type of ability, you wouldn’t be doing this in the first place.

Everything is shown together in a spreadsheet below. In separate posts, I’ll show you what formulas to use and how to put together your spreadsheet, but by no means should take this as gospel. Feel free to tailor this. Use what I show you as a base, follow it precisely, or completely ignore it – you have to end up with something in which you feel confident. And if you have suggestions, I’d love to hear about them in the comments (I hope I don’t regret saying that).

Below is a list of the critical inputs on which you’ll need to decide. I’ll give you what I use, and you can feel free to disagree.

- Starting age

- Starting savings

- Yearly contributions

- Annual rate of return

- Annual inflation rate

- Yearly deductions

- Yearly spending

First, another set of assumptions:

- I’m assuming that you pay your annual investment-related taxes until retirement out of your other income. If you pay your investment taxes out of your accumulated holdings, you’ll need to factor that into your yearly deductions category – and you’ll have to estimate how much you pay each year in taxes. It’s best if you do this as a factor of the amount of holdings, as the amount of taxes will undoubtedly increase as your holdings do. If you execute some precise tax-loss harvesting, estimate this as well. Secondary to this, after retirement, I’m assuming that the yearly spending includes taxes – meaning that if it says you’re spending $60,000 per year, in reality you’re probably spending about $40,000 – $45,000 per year with the rest going to taxes.

- Yearly deductions. You want to avoid this as much as possible while you’re saving, but some are inescapable. For example, if you’ve inherited an IRA and you’re required to take RMDs, you have to account for this because it will impact your balance, especially over the long-term.

- You may have to adjust the anticipated rate of return in later years if you adjust your portfolio to take on less risk. It’s not fair to assume the same rate of return on a less risky investment portfolio.

- This model does not take into account social security income. What was once a guarantee has become so precarious that I wouldn’t assume it’ll still exist in 10-20-30 years’ time. I know this is a big leap, but not entirely out of the realm of possible. Consider it a bonus if it’s still around when you retire.

- Finally, and this is a big one. I am calculating annual return on the closing balance of the prior year – meaning that in each year’s end total, I do not calculate gains on the money deposited during the year. The result is likely an underestimate of the total amount; however, the reason for this approach is to add a degree of conservatism due to the large fluctuations that can happen in the relatively short period of one year. Unless you make all deposits on the exact same schedule (which some will – if you do it with each biweekly paycheck) and the rate of return stays smooth over the year – which it won’t – eliminating this variable, even at the risk of undercounting, can help paint a better picture of the progression of your funds. This same assumption will apply to the period when you’re taking deductions, as I’ll explain further below.

I’ll add more permutations in future posts, but here’s an example with the following assumptions:

1. Starting age = 30

2. Starting savings = $100,000 in a 401(k)

3. Yearly contributions = $13,000 to brokerage account, $15,000 to 401(k) including match

4. Annual rate of return = 6%

5. Annual inflation rate = 2.5%

6. Yearly Deductions = 0 until needed

7. Spending = $5,000 per month in retirement

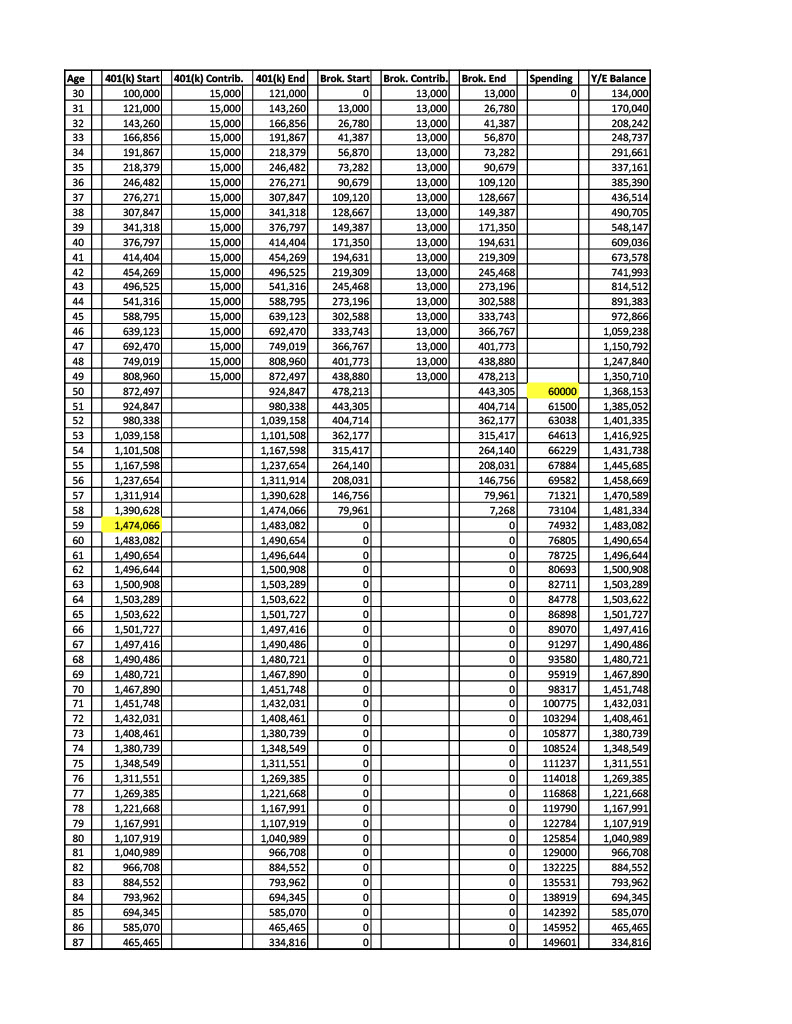

As you can see here, you start spending $60,000 per year at age 50, drawing only from the brokerage account, and avoiding the early withdrawal penalty that would be applicable if you withdraw money from the 401(k) before age 59 ½. The starting figure of $478,213 from the brokerage account is just enough to get you to age 59, at which point, the brokerage account is out of funds and you start drawing down the 401(k). Note that this permutation assumes that you turn 59 ½ the same year you turned 59 (i.e., your birthday is June 30 or earlier). If your birthday is July 1 or later, you’d either have to stretch the brokerage account another year or you would incur an early withdrawal penalty for taking money out of the 401(k) before the year you turn 59 ½.

As you can see here, you start spending $60,000 per year at age 50, drawing only from the brokerage account, and avoiding the early withdrawal penalty that would be applicable if you withdraw money from the 401(k) before age 59 ½. The starting figure of $478,213 from the brokerage account is just enough to get you to age 59, at which point, the brokerage account is out of funds and you start drawing down the 401(k). Note that this permutation assumes that you turn 59 ½ the same year you turned 59 (i.e., your birthday is June 30 or earlier). If your birthday is July 1 or later, you’d either have to stretch the brokerage account another year or you would incur an early withdrawal penalty for taking money out of the 401(k) before the year you turn 59 ½.

For this example, I’ve used a life expectancy of 87. By the time you hit 87 in this example, you still have money left in the 401(k), meaning that you made it to the end without running out. One thing to note here is that at age 72 (based on a new 2019 law), you have to start taking required minimum distributions (RMD) from your 401(k). Although not shown in the example, the amount you’d be taking out to meet your spending needs exceeds the applicable RMDs, so that doesn’t become a factor here. But, if you were taking out less from your 401(k), the RMD would kick in and mandate a certain minimum, which can accelerate depletion of the 401(k). Of course, you wouldn’t have to spend all of it – you could drop it right back into a savings account or investment account, but you’d still incur the taxes associated with the full deduction.

One thing you’ll also see here is that, for the sake of conservatism, once you start drawing down funds from the accounts, the assumption becomes that the 6% return accrues on the final balance for each year – that is, the starting balance less the full amount you spend over the year. This undercounts the return in some respects, similar to the way that in the “savings” years, the return is only calculated on the starting balance and does not factor in the contributions over the year. The effect of this assumption is more pronounced in the spending phase because you’re taking out more money than you were putting in during the “saving” phase (e.g., spending greater than $60k each year vs. max $28k in contributions), so there’s a greater share of excluded funds from the return-generating calculation. My suggestion is to treat this as a little extra safety blanket.

Note also that most 401(k) savers put their money into a target-date retirement fund. As you get closer to the target date, the asset balance shifts to a less risky profile, which in turn generally means a lower rate of return. Given the conservative estimates baked into this model, including the assumption of a general 6% return rate, I haven’t reduced the rate of return for the latter years of the 401(k). If you want to add another level of comfort to this model, you might start reducing the return rate depending on the target date of the fund in which your money is invested.

This is just one example. It assumes that you’ve built up some retirement savings before you decide to start pursuing FIRE, that you’re able to start saving $28,000 per year toward FIRE at age 30, and that you retire at 50. In this example, you’re able to do it, so long as you can keep your spending to $5,000 per month in retirement, adjusted for inflation. In later examples, I’ll show what happens if you save more or less, and what happens when you’re able to generate some wage income in retirement.

I won’t obscure the fact that this model is very basic, and gives you a rough idea of what you can expect. The financial-modeling inclined might add more variables and factors, or adjust the linearity of the returns. By all means, if you’re trying to figure out if you’ll have enough money, do whatever you need to do to feel comfortable. After all, the primary consideration here should be to avoid running out of money at a time when it’s no longer possible to work.