The 401(k). That thing your employer uses as an incentive to help you retire, and perhaps the most common place people working in the private sector store away their wages for retirement. But how much do you actually know about how those funds are invested, how much it costs you for the privilege, and what exactly you’re doing with your money?

As I’ve said elsewhere, a 401(k) offered by your employer can be an invaluable part of investing toward an early retirement, or any retirement, for that matter. This is particularly so if your employer makes a contribution on your behalf, such as when an employer offers matching or just deposits an amount each year in your account. Assuming you take advantage of what your employer offers, this is a nice little salary bump, even if you don’t see the benefits of it for years down the road. With compounding returns, the little bump can turn out to be worth much more over a long investment term, so don’t sell it too short. An extra $2-3 thousand per year over 20-30 years can result in compound returns that amount to over six figures.

Employers frequently offer these plans and provide the required disclosures, but I’d bet a fair wager that it’s only a small portion of people who actually dive into how their money is being invested. Disclosures are couched in investment-speak, and for the most part only refer to other investments (as in, the investments in which your 401(k) fund puts its money), so there are multiple layers of work to do if you really want to know where your funds are going.

The good news is, for the most part, that 401(k) funds can earn a decent return over the long-run, much like the stock market generally. Or, at least, this is what history has shown. However, that doesn’t mean you should rest on your laurels thinking everything is all set and you don’t have to think about it. So, with that, let’s look a little deeper at 401(k) accounts.

Brokerage Firms

Employers that offer a 401(k) will partner with a financial management company to serve as the administrator of the account. You might recognize the names of these companies from your own investing or from commercials you see on tv – for the most part, large employers strike deals with the major brokerages: Fidelity, T. Rowe Price, TD, JP Morgan, etc. Not all companies work with the big names, however, particularly smaller employers that may have arrangements with lesser-known financial management firms. Regardless of name or ubiquity, these firms hold your money and invest it on behalf of the employer’s 401(k) contributors.

Once your money is deposited in the firm’s account, you should be able to use its infrastructure (app, website, paper statements…) to look up your balance, make changes in the amount you divert from your paychecks, see how your money is invested, and see how it’s performing.

Target Date Funds

The bulk of 401(k) providers offer what’s called target date funds. The way target date funds work is that the employee (you) chooses the year of the fund closest to their anticipated retirement date and their 401(k) payroll deferrals are invested in that fund. Most large firms offer target date funds in five year increments, so, for example, you’ll see funds with target dates of 2030, 2035, 2040, 2045, and so on. Some companies will, by default, invest your money into the fund with a target date closest to the year you turn 65, but will allow you to change the fund by following whatever procedure they need you to do.

These funds operate similar to mutual funds. The fund is managed and invests in a portfolio of assets (stocks and bonds) and each time you buy in, you acquire shares corresponding to a portion of the fund’s underlying value, which is determined by the value of the assets the fund holds. For example, if the fund holds stocks and bonds with a market value on a particular day of $100 million, and there are 50 million shares outstanding, each share is worth roughly 2 dollars. When you contribute $500 from your paycheck, you acquire 250 shares of the fund on that day.

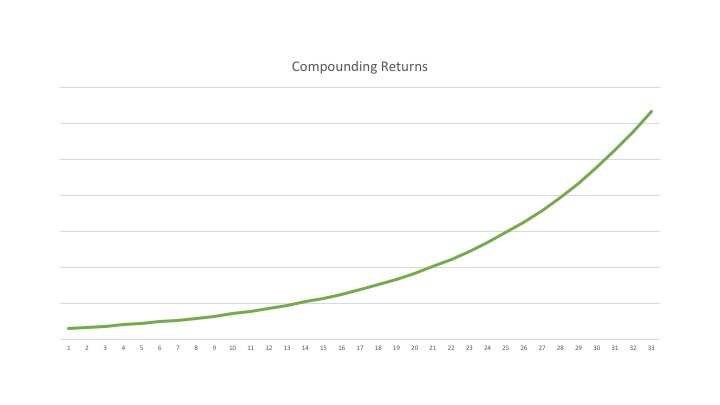

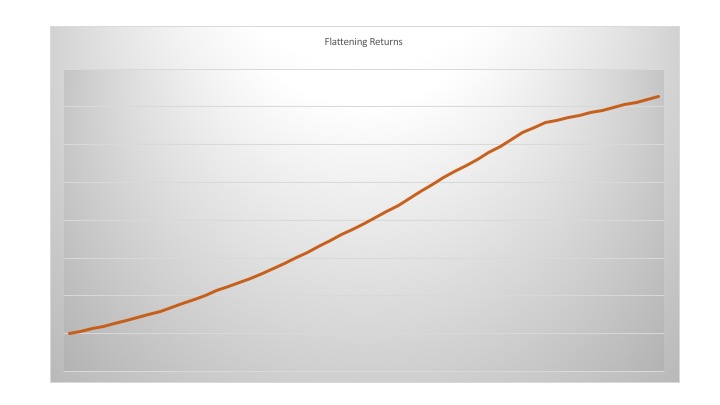

What makes target date funds unique is that they adjust the risk profile of the fund as the “target” date approaches. Further out from the target date, when its investors are theoretically younger, the fund will generally hold more equities for their higher return, on the theory that the further someone is from retirement, the more risk they can tolerate. As the target date approaches, the investment balance shifts toward less risky assets like bonds, which reduces the risk of the investments and the corresponding potential for volatility. The theory here is that as you approach retirement, you take on less risk because you have less time to make back losses if there’s a downturn.

A high level example is as follows. Assume you start working at age 22 in 2020, and plan to retire at age 65. You might invest in a target date fund for 2065, which is closest to your target age. In year 2020, the fund might be invested 85% in stocks and 15% in bonds, taking on a stock-heavy risk profile at an age when it’s unlikely you’ll need (or want) to withdraw money. By doing this, the fund looks to capture the potential value increase from holding stocks, but also has some security with the partial investment in bonds. In year 2050, the profile might look a little different. By then, it might be 60% stocks and 40% bonds, reducing the risk but still capturing the returns that equities can offer.

By 2060, the investment makeup might be 25% stocks and 75% bonds, a significant reduction in risk as you approach retirement and a time when you might start living off the money and are no longer able or willing to tolerate the risk of a downswing. In year 2065, as you look back at the historic returns, you’ll see that the fund was subject to greater volatility in its earlier years, but likely produced a higher rate of return. In latter years as the target date approached, there was less volatility but the rate of return declined. At least, this is what target date funds intend to accomplish.

Overall, not a bad concept. Indeed, it absolutely makes sense to take on more risk when you can tolerate it and less risk when you should be playing it safer. Target date funds capture this risk profile for you, allowing you to invest without having to think about it too much. Done right, it’s a great way to save for retirement.

Other Considerations

So, what’s the downside? First off, those target date funds, like mutual funds, do not come free. If you read through the disclosures your employer and/or the fund provides you, there are plenty of baked-in fees for the management of the fund. These fees will come in the form of direct fees, i.e., debits from your balance, or in the form of diminished value of the fund that goes to management costs. For example, if the underlying assets at the close of the day are worth $10 million and there are 10 million outstanding shares, each share will not be worth $1, but will be worth, say 99 cents, with the other 1% going to management fees. Each fund is different, so you have to check the paperwork.

Second, target date funds are likely to skew toward the conservative side of investing – even in those years when the funds are heavily invested in equities with the “target” retirement date a ways off. The reason why is fairly self-explanatory: large employers are unlikely to direct their employees’ assets toward funds that have a track record of losing money. While average returns are palatable, losses do not sell too well, particularly when employees focus only on whether the fund goes up or down, and not how well it tracks general market movement. Simply the prospect of a loss, or a historical loss (even if gained back) can look bad, leading many of the large funds to try to protect against taking losses.

Now, I’ll add the caveat that this varies massively by fund. There are many many funds out there, each with its own investment mix and management style. Some may have returned higher than others and some lower. When you’re investing your 401(k), each fund is required to provide a disclosure statement that lists, among other things, where the fund invests its assets and historical returns. If you review this information, you can gain an understanding of the sort of risk that the fund takes on by looking at, for example, the stock/bond ratio, the types of stocks invested in (old blue chips vs. riskier stocks, like tech), the types of bonds (all rated AAA or with some lower rated in the mix), and so on. But, what I’m saying is that if you review this information, you’ll tend to see investments that, based on their history, have less likelihood of failing, and potentially, correspondingly lower rates of return.

What this means is that even when the fund is investing in “riskier” assets, you’re potentially not taking on as much risk as you can tolerate, and in the process foregoing some of the potential for higher returns. If you’re 25 and don’t plan to retire until you’re 45 (or 60), you can get pretty risky, at least as far as investing in the stock market can get. Remember, the chances of you getting completely wiped out in the stock market are fairly slim, especially with a long-range horizon. (Other investments can certainly wipe you out, but they’re more difficult to find and probably not as available through the stock market).

And, as the target date approaches, the fund – by design – is going to become even more conservative, to the point where your returns are getting fairly minimal and potentially hovering slightly above inflation.

Target-Date Funds for the FIRE Investor

So what does this mean for a FIRE investor?

Generally speaking, target date funds are not a bad idea – in fact, they’re pretty good for your average investor. But, this assumes that the 401(k) is essentially your only source of retirement investing. And, for many people, it is. Which is why I look upon target date funds highly. They help people achieve a suitable allocation risk for a reasonable price.

But, if you’re investing for FIRE, your 401(k) is not going to be your only source of retirement investments. In fact, I dare say that there’s no way to get to FIRE with only a 401(k) given the limits on yearly contributions. If you plan to retire at 45, even if you start at 22 and max out the contribution every year, you’ll end up with somewhere between $900k to $1 million if the historical average of 6-7% annual returns holds, which probably isn’t going to be enough unless you spend your remaining years living an extremely thrifty lifestyle.

Because a 401(k) may not be the FIRE investor’s only source of retirement funds, a target date fund may be a little too conservative given that you have additional money as a fallback. Unlike someone whose only retirement funds are in a 401(k), a FIRE saver may be able to take on a little more risk because there is less chance of a major setback in the event of a downturn.

Moreover, if you’re investing properly for FIRE, you should be diversifying on your own, with a healthy mix of risk. Adding a target date fund may skew your overall portfolio more conservative than it needs to be. You may also be subjecting yourself to management fees that you can avoid if you’re able to manage your own investments.

But let’s be clear. I’m not saying that FIRE savers should avoid investing in target date funds. In fact, they can play an important role in your overall strategy.

Primarily, you can use a target date fund as a hedge for your longer-term needs. If you’re planning to retire at 45, you won’t be using your 401(k) to live off for at least another 15 years or so to avoid the early withdrawal penalty for taking distributions before age 59 ½. You can leave the 401(k) and let it grow, even if you’re not contributing to it anymore. It’ll be there when you need it as the balance of your non 401(k) accounts start to dwindle (if it does). Although, see below for a further discussion of what you can do with your 401(k) once you retire.

If you do decide to keep your money in a 401(k) while you’re retired, you might consider selecting a target date fund with a target date well beyond your 65th birthday. If you have enough risk balance in your non-401(k) investments, or if you think you have enough non-401(k) funds to last beyond 65, then you might not need the reduction in risk that would come as the target date approaches. Rather than letting that risk taper, along with your expected returns, you can maintain a more equity-heavy investment portfolio in the 401(k) for longer by choosing a date that’s further in the distance.

You might also consider the strategy of picking a target date that’s beyond your 65th birthday while you’re still working. If you’re investing in a 401(k) while you’re working, and decide to use the target date funds your employer offers, then picking a date that’s further out should result in a fund in its earlier years that skews more heavily toward equities. This strategy can help overcome some of the natural conservatism that comes with investing in a target date fund.

Of course, there is the alternative not to invest in a target date fund at all. Some employers will allow you to self-direct your 401(k), meaning that the money is deposited into your account and you use it to purchase whatever combination of assets offered by the management firm. This gives you greater control over the risk in your account, but does of course mean that you have to pay closer attention to it. Also be sure to determine whether you’d face commission charges from self-directed investing – these can add up over time.

Leaving Your Employer

Another thing to keep in mind about 401(k) investing is that when you leave your employer, you have the opportunity to take your money out of the 401(k) and self-direct your retirement account.

If you have a high enough balance, your former employer may allow you to leave your money in the 401(k) even though you no longer work for them. Typically you’ll only have this option if you have at least $5,000 in the employer’s 401(k). But, even if you have this option, you don’t have to leave your money there. You can roll it into your new employer’s 401(k) if they offer one, or you can roll it into an IRA of your choice.

In fact, rolling an old 401(k) into an IRA is a great way of converting pre-tax money to a self-directed IRA all at once. In a given year, you’re subject to limitations on how much you can put into an IRA, and if your income is over a certain level and your employer offers a 401(k), you’re not able to take advantage of deferring taxes on the money deposited. But rolling an old 401(k) into an IRA is not subject to limitations on amount, allowing you the freedom of investing the money however you desire instead of being limited to what you can do within the confines of an employer-sponsored 401(k). You can do this any time you change jobs, or when you retire for good.

One thing you likely don’t want to do is to cash out your 401(k) when you leave an employer. If you were to do this, you’ll incur taxes on the entire amount as though it were ordinary income, and this can wipe out a large portion of what you’ve invested for no good reason. So to the extent you can, avoid cashing out. Either keep the funds where they are, or roll them into an IRA or new 401(k) and you won’t face any unnecessary taxes.

If you do elect to rollover an old 401(k), make sure you do it properly to avoid mistakenly subjecting your distribution to taxes. As of the date of posting, you have 60 days to make a rollover without facing taxes for the distribution, and you have to make the rollover into a qualified retirement account – such as an IRA. Once the money is in the IRA, you’re free to invest as you please, and the money can continue to grow without facing interim taxes so long as you don’t make any withdrawals before age 59 ½.

Conclusions

A target date fund offered through a 401(k) is a convenient way to save for retirement, and for most investors, is a great way to achieve a suitable risk profile without having to think about it.

But, for the FIRE investor, like everything else, you should think about whether it’s too conservative for your investment strategy or whether you’re unnecessarily incurring management fees. Remember that there are alternatives, whether choosing a riskier target date fund or self-directing the money in your 401(k). The point is, if you’re using the 401(k) as one of your strategies to invest for retirement – and indeed, you probably should – don’t take the default route without giving it some consideration. You might find that you can do better.